If you've been watching the Canadian condo market lately, you've probably noticed things look a little rough.

Toronto's condo market in particular has been in a full-blown correction and it's not just a blip. It's one of the biggest stories in Canadian real estate right now, and whether you're a buyer, seller, investor, or just a curious homeowner, it affects you.

Let's break it down.

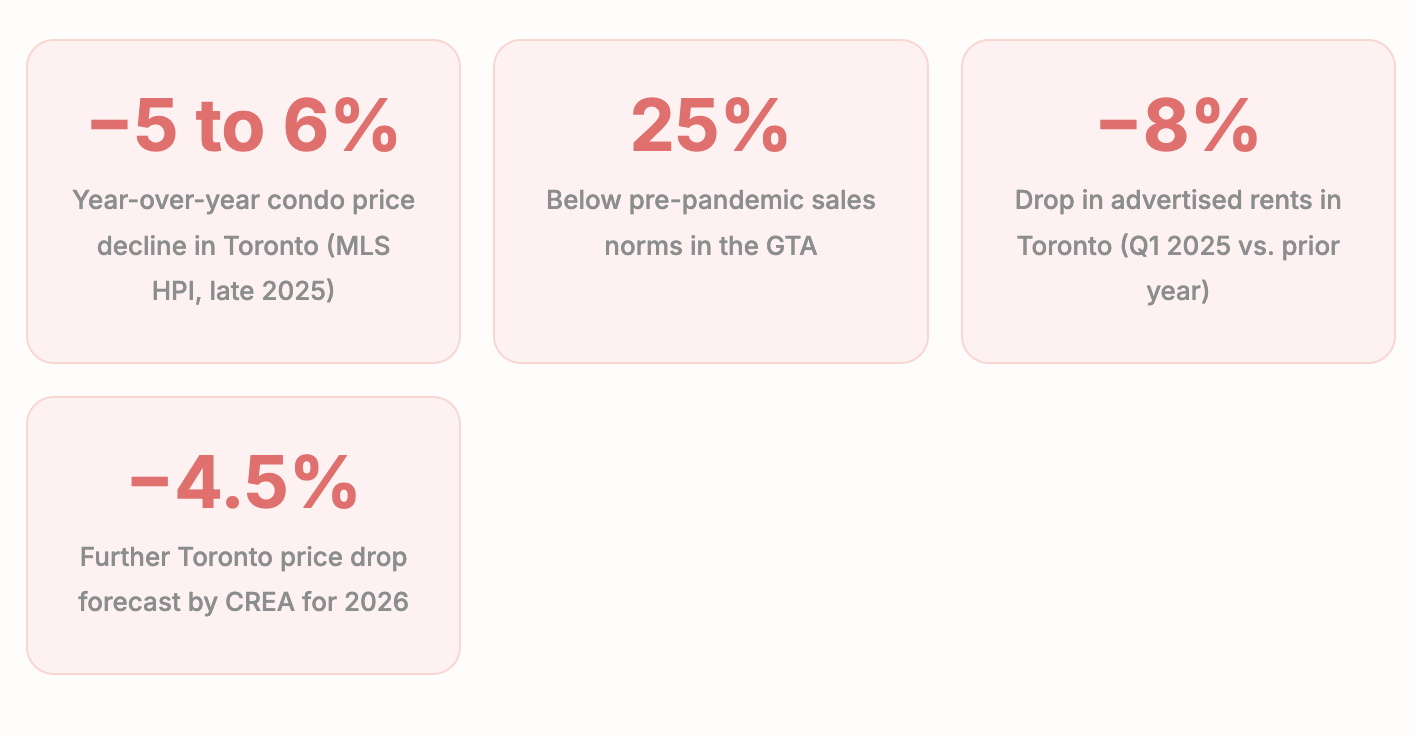

The Numbers Don't Lie

These aren't projections. Most of these numbers are already baked into the market. Buyers have the upper hand right now, and that's a pretty significant shift from just two or three years ago.

So, What Actually Happened?

A few things collided at once to create this mess:

1. Investors flooded the market with listings

During the pandemic, a huge wave of investors snapped up preconstruction condos at sky-high prices, expecting rents to keep climbing and values to keep rising. When interest rates spiked in 2022 and 2023, carrying costs shot up, rents softened, and resale prices started falling. Many investors decided to cut their losses — and suddenly the market was flooded with supply at exactly the moment buyer demand was weakest.

2. Rate shock hit hard

Buyers who qualified for mortgages at 2% are now renewing or qualifying at 5%+. That's not a small adjustment — in many cases it meant hundreds of extra dollars per month. Demand fell off a cliff.

3. Economic uncertainty put everyone on pause

US tariff threats, slower immigration, a cooling job market — none of this inspired confidence. A lot of potential buyers and sellers just… waited. And many are still waiting. The Bank of Canada brought its overnight rate down from 5.0% all the way to 2.25% by late 2025 — a significant easing cycle. But so far, it hasn't been enough to reignite condo demand in Ontario's major markets.

Who's Hurting — and Who's Actually Winning

The ones feeling the pain

Preconstruction buyers are arguably the hardest hit. Many signed agreements at 2021–2022 peak prices, and are now closing on units worth less than what they paid — while also facing higher mortgage rates than they originally projected. In some cases, buyers are walking away from deposits entirely.

Condo investors who were relying on price appreciation or rental income to cover carrying costs are squeezed. Rents have softened and values have dropped, creating a painful double hit.

The ones with an opening

First-time buyers and end users (people who actually want to live in the unit) are in the best buying position they've been in years. Prices are lower, inventory is high, sellers are negotiating, and conditions are back. The REIC projects that in Toronto, the average monthly mortgage payment on a benchmark condo will fall in 2026 for the first time since 2020.

Renters also benefited — advertised rents dropped 2–8% in major cities through early 2025, giving some relief after years of brutal increases.

Regional Markets Tell a Very Different Story

The condo crisis is largely concentrated in Ontario (especially the GTA) and to a lesser degree in BC. But elsewhere? The picture looks very different.

Quebec City saw 12% year-over-year price growth in 2025, driven by tight supply and a cultural shift toward homeownership. Saskatchewan posted 9% average home price growth. Regina is running at a 50% absorption rate three times what a "normal" market looks like. These markets are effectively the opposite of the Toronto condo crash.

Canadian real estate" is not one market. If you're making decisions based on national headlines, you might be working with the wrong map entirely.

What Happens Next?

Most forecasters are expecting a modest, gradual recovery rather than a sharp rebound. Here's the consensus view heading into 2026:

National home sales are projected to rebound by about 5.1% in 2026, and average prices are expected to edge up roughly 2.8% nationally — though Ontario and BC will likely see prices continue to drift lower in the first half of the year before stabilizing. The Bank of Canada is expected to hold rates steady, which means the mortgage relief that buyers are hoping for may be more limited than expected.

The wild card? US tariffs and their ripple effects on Canadian employment and consumer confidence. If the economic picture darkens further, all bets are off. If it stabilizes, pent-up demand — and there's a lot of it — could start flowing back into the market by mid-2026.

If You're Thinking About Buying a Condo Right Now...

Here's our honest take: this is a market where preparation and legal protection matter more than ever. With prices still moving around, preconstruction deals getting complicated, and closing conditions shifting, you want to make sure you understand exactly what you're signing — and what it'll cost you to close.

A few things worth knowing before you move forward:

✅ Always review your Agreement of Purchase and Sale carefully — especially any assignment or termination clauses.

✅ Understand your closing costs upfront — they're not just lawyer fees.

✅ If you're buying preconstruction, pay close attention to what happens if you can't close (or don't want to).

✅ Get your mortgage pre-approval locked in before making an offer.

Related Reading from Deeded

- How Much Does a Real Estate Lawyer Cost in Ontario?

- Real Estate Legal Documents — What You'll Need to Sign at Closing

- What is a Statement of Adjustments and How to Read One

- The Potential Effects of Trump's Tariffs on Canada's Real Estate Market

- Independent Legal Advice (ILA) — And When You May Need It

Unlock Your Seamless Closing Experience

Your Journey to a Worry-Free Closing Starts Here!