By Deeded.ca | Last updated: March 25, 2026

TL;DR: Ontario and the federal government are combining to eliminate up to $130,000 in HST on newly built homes. Ontario announced on March 25, 2026 that it's expanding its HST rebate to all buyers — not just first-time buyers — for one year, covering the full 13% HST on new homes up to $1 million. This builds on the federal First-Time Buyer GST Rebate (Bill C-4), which already eliminates the 5% federal GST for eligible first-time buyers. For first-time buyers of new construction in Ontario, this is now the largest tax incentive in a generation.

Buying a newly built home in Ontario just got significantly cheaper.

On March 25, 2026, Premier Doug Ford announced that Ontario will eliminate the full 13% HST on new homes valued up to $1 million for a one-year period beginning April 1, 2026. The move expands eligibility beyond first-time buyers to include all purchasers, including investors buying rental properties.

This provincial announcement builds on the federal First-Time Buyer GST Rebate introduced through Bill C-4, the Making Life More Affordable for Canadians Act, which received Royal Assent on March 12, 2026. Together, the two programs create a combined rebate of up to $130,000 on a single new home purchase.

Here's everything you need to know about both programs, who qualifies, and how much you could save.

Two Programs, One Goal: How the Federal and Ontario Rebates Work Together

There are now two distinct programs working in tandem to reduce or eliminate the HST on new homes in Ontario. Understanding how they interact is important because their eligibility rules differ.

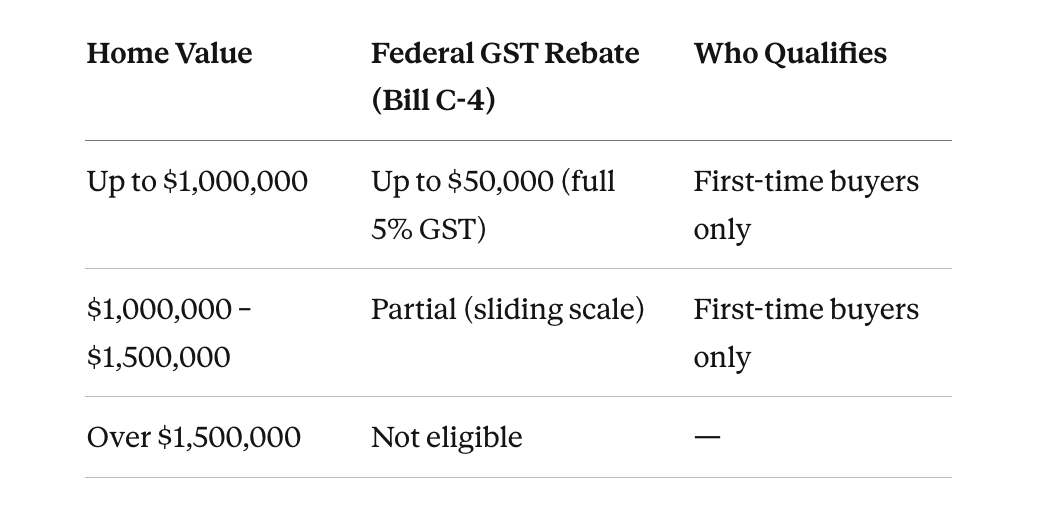

The federal First-Time Buyer GST Rebate (Bill C-4)

Eliminates the 5% federal portion of the HST on newly built homes for eligible first-time buyers. It applies to homes priced up to $1 million (full rebate) and offers a partial rebate on homes between $1 million and $1.5 million.

The program covers agreements signed between March 20, 2025 and December 31, 2030. According to the Department of Finance Canada, the maximum savings are $50,000.

Ontario's expanded HST rebate

Eliminates the 8% provincial portion of the HST on new homes for all buyers (First-time or not) for a one-year period. It applies to purchase agreements signed between April 1, 2026 and March 31, 2027.

For the one-year window, the Ontario and federal governments are also partnering to cover the federal 5% GST for all buyers (not just first-time buyers), meaning the full 13% HST is eliminated.

For first-time buyers, both programs stack automatically. For non-first-time buyers, the one-year Ontario expansion provides the combined 13% relief directly through the federal-provincial cost-sharing agreement.

Calculate your Eligibility for the Federal and Ontario HST Homebuyer Rebate

There are many details and criteria for both the Provincial and Federal rebates, so we thought why not build a simple calculator tool to help you understand your potential eligibility. Since the programs are new and could change, this tool is for informational purposes only and does not constitute legal, tax, or financial advice. We do not guarantee the accuracy of the estimates provided. Actual savings may differ. Program details, eligibility criteria, and rebate amounts are subject to change at any time by federal or provincial governments. We strongly recommend consulting a Real Estate, Legal, or Tax professional PRIOR to entering any agreement.

How Much Can Homebuyers Save?

The savings depend on the price of the home and whether you're a first-time buyer.

Outside the one-year Ontario window, the federal First-Time Buyer GST Rebate continues to apply on its own for eligible first-time buyers:

To put this in practical terms: a first-time buyer purchasing a $900,000 newly built home in Ontario between April and March 2027 would save approximately $117,000 in HST. That's more than many buyers put toward a down payment.

Who Qualifies for the Ontario HST Rebate?

For the one-year expanded period (April 1, 2026 to March 31, 2027), Ontario's rebate is open to all buyers This is a significant departure from the previous program, which was limited to first-time purchasers. Eligibility criteria include:

- Purchase agreement must be signed between April 1, 2026 and March 31, 2027

- The home must be a newly built or substantially renovated property

- The home must be used as a primary residence or a residential rental property

- For primary residences, construction must begin on or before December 31, 2028 and be substantially completed on or before December 31, 2031

- For rental properties, construction must be substantially completed on or before December 31, 2029

- If construction began before March 31, 2026, the purchase agreement must be signed between April 1, 2026 and March 31, 2027, and construction must be substantially completed by December 31, 2029

The province has noted that additional eligibility criteria will be posted on Ontario.ca by the end of March 2026.

Who Qualifies for the Federal First-Time Buyer GST Rebate?

The federal rebate under Bill C-4 has its own eligibility criteria. To qualify, you must meet all of the following:

- You must be at least 18 years old at the time of purchase

- You must be a Canadian citizen or permanent resident

- You must not have owned and occupied a home as your primary residence during the current calendar year or the four preceding calendar years

- The property must be intended as your primary place of residence

- You must be the first person to occupy the home after construction or substantial renovation is complete

- The home must be a newly built or substantially renovated property

- Your agreement of purchase and sale must be entered into on or after March 20, 2025 and before January 1, 2031

This definition is consistent with how "first-time buyer" is interpreted across other federal programs like the Home Buyers' Plan (HBP) and the First Home Savings Account (FHSA), so if you've qualified for those, you'll likely qualify here too.

What About Investors and Rental Properties?

One of the most notable aspects of Ontario's announcement is that the expanded rebate explicitly covers residential rental properties. This is designed to encourage purpose-built rental construction, which has been one of the weakest segments of new housing supply in Ontario.

The federal First-Time Buyer GST Rebate does not cover investment or rental properties — it requires the buyer to occupy the home as their primary residence. However, during the one-year Ontario window, investors purchasing new rental properties can still access the combined 13% rebate through the federal-provincial cost-sharing arrangement.

How Do I Claim the HST Rebate?

For transactions closing after the programs take effect, both rebates are designed to be applied at closing. Builders can credit the rebate directly on the statement of adjustments, reducing the amount you owe at closing. The builder then claims the rebate from the CRA on your behalf.

For the federal First-Time Buyer GST Rebate on transactions that closed between March 20, 2025 and March 12, 2026 (before Royal Assent), buyers need to apply directly to the CRA to claim the rebate retroactively. According to the Canada Revenue Agency, rebate claims have been processed since Royal Assent on March 12, 2026.

When purchasing a new home, ask your builder whether the rebate will be reflected on your statement of adjustments. Your real estate lawyer should confirm the amounts at closing.

Does the HST Rebate Apply to Resale Homes?

No. Both the federal and Ontario rebates apply exclusively to newly constructed homes and substantially renovated properties. Resale homes are not subject to GST/HST and are not eligible for these programs.

Can I Combine the HST Rebate with Other Incentives?

Yes. The federal First-Time Buyer GST Rebate is a separate program and can be used alongside:

- The Home Buyers' Plan (HBP), which allows first-time buyers to withdraw up to $60,000 from their RRSP for a home purchase

- The First Home Savings Account (FHSA), which combines tax-deductible contributions with tax-free withdrawals for a first home

- The First-Time Home Buyers' Tax Credit, a $10,000 non-refundable credit worth up to $1,500 in tax savings

Ontario's expanded rebate stacks on top of all of these for buyers who qualify.

How Will This Affect the Housing Market?

Both programs are targeted at new construction, which is a deliberate policy choice. By incentivizing purchases of newly built homes, the federal and Ontario governments aim to stimulate housing supply, one of the root causes of Canada's affordability crisis.

Ontario estimates the expanded HST rebate alone could stimulate an additional 8,000 housing starts, support up to 21,000 jobs, and boost real GDP by $2.7 billion. The combined federal-provincial relief is valued at nearly $2.2 billion.

Data from the Canadian Real Estate Association shows that inventory shortages remain a persistent challenge in major markets, and more demand for new builds should encourage more construction starts. For a deeper look at where the market stands today, see our February 2026 Canadian real estate market recap.

That said, demand-side incentives can also push prices higher if supply doesn't keep pace. Buyers should be realistic about current market conditions and avoid overextending simply because of the tax savings. The rebate is substantial, but it doesn't change the fundamentals of what you can afford on your monthly budget.

What Should Buyers Do Next?

If you're considering a new build in Ontario, here are the practical steps to take now.

First, determine which programs you qualify for. If you're a first-time buyer, you're eligible for both the federal GST rebate and Ontario's expanded HST rebate — up to $130,000 in combined savings. If you're not a first-time buyer, you can still access the full 13% rebate during the one-year Ontario window (April 2026 to March 2027).

Second, pay attention to the agreement dates. For Ontario's expanded rebate, your purchase agreement must be signed between April 1, 2026 and March 31, 2027. For the federal rebate, the window extends until December 31, 2030.

Third, ask the builder about closing mechanics. The rebate should be credited on your statement of adjustments, but confirm this in advance. Be sure to also read the fine print on any developer price guarantees.

Fourth, talk to your real estate lawyer. With two overlapping programs, different eligibility criteria, and specific construction deadlines, having a legal professional review the details at closing is important.

With the broader shifts making 2026 a potentially strong year for buyers, up to $130,000 in combined HST relief, and multiple federal incentive programs available, buyers of new construction in Ontario have a tangible financial advantage worth planning around.

Frequently Asked Questions

How much HST can I save on a new home in Ontario in 2026?

If you're buying a newly built home in Ontario priced at $1 million or under, you could save up to $130,000 — the full 13% HST. This combines Ontario's 8% provincial portion and the federal 5% GST. The maximum $130,000 rebate applies to homes valued up to $1.5 million. For homes between $1.5 million and $1.85 million, the rebate decreases proportionally. Homes above $1.85 million receive $24,000 under the pre-existing rebate.

Do I need to be a first-time buyer to get the Ontario HST rebate on a new home?

For the one-year period from April 1, 2026 to March 31, 2027, no — Ontario has expanded eligibility to all buyers, not just first-time buyers. However, the federal First-Time Buyer GST Rebate (Bill C-4) that covers the 5% federal portion is limited to first-time buyers. During the one-year Ontario window, non-first-time buyers still receive the full 13% through the federal-provincial cost-sharing agreement.

Does the Ontario HST rebate apply to rental properties?

Yes. Ontario's expanded HST rebate covers both primary residences and residential rental properties. For rental properties, construction must be substantially completed by December 31, 2029.

When does the Ontario HST rebate for new homes start and end?

The expanded rebate applies to purchase agreements signed between April 1, 2026 and March 31, 2027. For primary residences, construction must begin by December 31, 2028 and be completed by December 31, 2031. For rental properties, construction must be completed by December 31, 2029.

Can I combine the federal First-Time Buyer GST Rebate with Ontario's provincial HST rebate?

Yes. The federal First-Time Buyer GST Rebate (Bill C-4) covers the 5% federal GST, and Ontario's expanded rebate covers the 8% provincial portion. Together they eliminate the full 13% HST on eligible new homes. The federal rebate is limited to first-time buyers; Ontario's temporary expansion is open to all buyers.

Does the HST rebate apply to resale homes?

No. Both the federal and Ontario rebates apply exclusively to newly constructed homes and substantially renovated properties. Resale homes are not subject to GST/HST and are not eligible for these rebates.

Can I get the federal rebate if I already closed before Bill C-4 became law?

Yes. If you signed your purchase agreement on or after March 20, 2025, and your closing took place before March 12, 2026 (Royal Assent), you are still eligible. You'll need to apply directly to the CRA to claim your rebate retroactively.

Can I combine the HST rebate with the Home Buyers' Plan or First Home Savings Account?

Yes. The HST rebates are separate from the Home Buyers' Plan (HBP), the First Home Savings Account (FHSA), and the First-Time Home Buyers' Tax Credit. All can be used together.

Unlock Your Seamless Closing Experience

Your Journey to a Worry-Free Closing Starts Here!

.jpg)