The Toronto and GTA condo market is experiencing its most severe downturn in over 30 years, with sales at 28-year lows, record inventory levels, and widespread project cancellations signaling a fundamental market reset. New condo sales plummeted to just 4,590 units in 2024—a 64% decline from 2023 and the lowest volume since 1996. This collapse represents far more than a typical cyclical correction; it's the unwinding of nearly a decade of speculation-driven growth that peaked during the pandemic boom.

The crisis stems from a perfect storm of factors: aggressive interest rate hikes that more than doubled borrowing costs, massive oversupply from pandemic-era construction completions, and the retreat of investors who comprised over half of the pre-construction market. Industry experts unanimously predict continued weakness through 2025 with price declines of 15-20% from peak levels, followed by a gradual recovery beginning in 2026. However, the current collapse is simultaneously creating the foundation for a severe housing shortage by 2026-2027, as construction starts have fallen 88% below historical averages.

This analysis provides real estate professionals and potential buyers with the comprehensive data and forward-looking insights needed to navigate this unprecedented market environment and position for the eventual recovery.

Market performance hits historic lows across all metrics

The scale of the current market collapse is evident in every key performance indicator. Total condo sales dropped 21.7% year-over-year in Q1 2025 to just 3,794 transactions, while new construction sales reached their lowest quarterly volume since 1995 at only 533 units. Average selling prices have declined from a peak of $790,398 in Q1 2022 to $680,146 in Q1 2025, representing a 14% decline from peak levels with further drops expected.

The supply-demand imbalance has reached extreme proportions. Toronto condos currently face 7.85 months of inventory, the highest level in five years—while the broader market sits on nearly 40,000 unsold units across new construction, assignments, and resale properties. At current sales pace, it would take over 50 months to absorb this inventory, compared to the 14-16 months considered balanced market conditions.

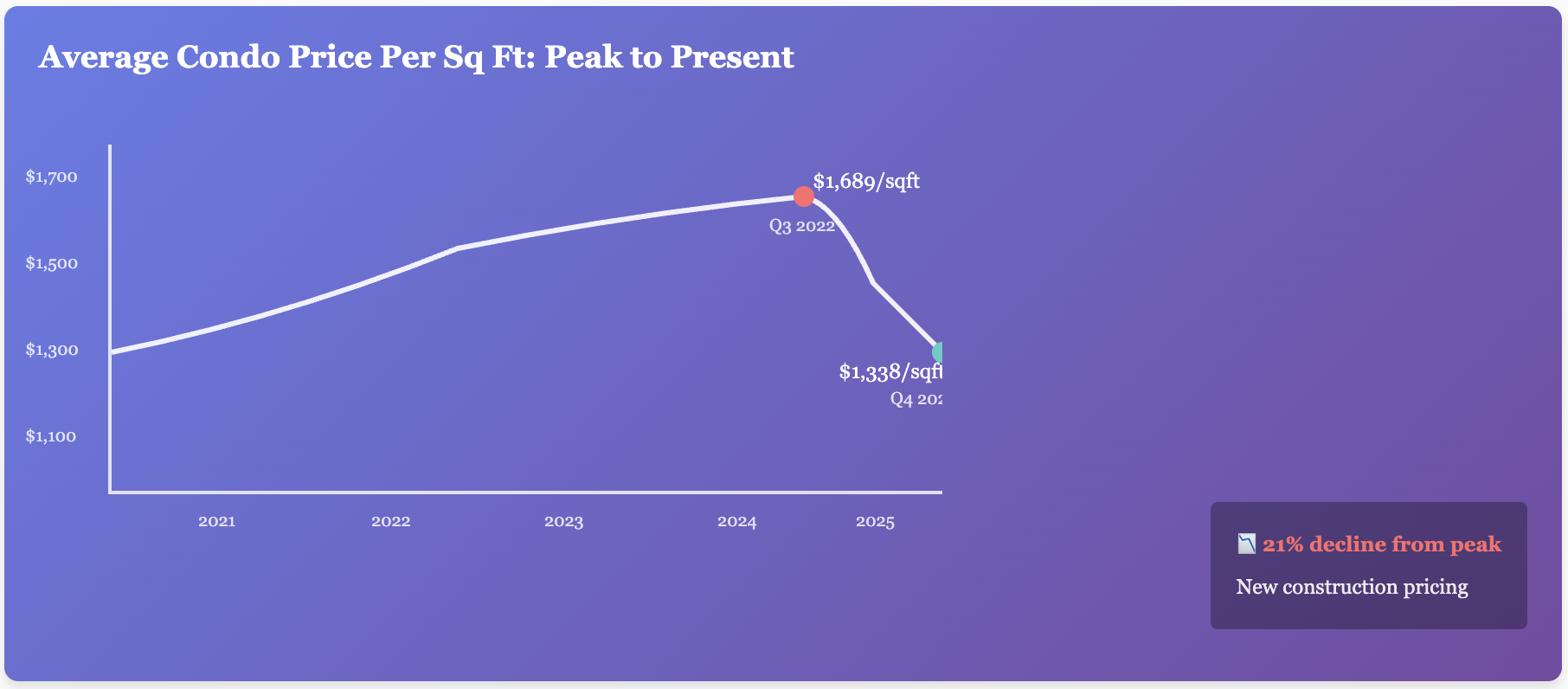

Price per square foot data reveals the depth of the correction. New construction units that peaked at $1,689 per square foot in Q3 2022 are now selling for $1,338 per square foot in Q4 2024—a 21% decline. Resale condos are trading at $813 per square foot, down from recent peaks, while new project launches are pricing units at just $1,151 per square foot to attract scarce buyers.

Construction activity has virtually ceased, with only 497 units starting construction in Q1 2025—an 88% decline below the 10-year average. This represents the lowest quarterly construction start since 1996, signaling a complete halt to new development activity. Meanwhile, record completions continue to flood the market, with 31,396 units expected to complete in 2025, surpassing 2024's already-record level of 29,671 units.

Project cancellations and developer distress reach unprecedented levels

The developer community faces its most challenging environment since the 1990s recession, with 14 condo projects cancelled in 2024 totaling 2,805 units—the highest cancellation volume since 2020. An additional 4 projects representing 1,042 units were cancelled in Q1 2025 alone, while 33 projects totaling 6,796 units have been either cancelled, converted to rental, put on hold, or placed under receivership over the past two years.

The most notable recent cancellation involves Birchley Park, an 860+ unit project by Diamond Kilmer Developments in East Toronto, which launched at $1,191 per square foot in April 2023—significantly above comparable resale prices in the area. The project's failure highlights the fundamental disconnect between developer pricing needs and market reality, with nearby Linx condos selling for $850 per square foot, 28% below Birchley Park's launch pricing.

High-profile receivership cases underscore the sector's financial distress. The One tower at Yonge and Bloor represents the most significant developer insolvency, with Mizrahi Developments defaulting on $1.23 billion in loans after total project debt reached $1.6-1.7 billion. Construction stalled at approximately 40 storeys, with completion now delayed from 2022 to 2025 at earliest. Other major receivership cases include Sanctuary Lofts ($42 million debt), multiple Maplequest Ventures projects ($90 million debt), and several StateView Homes developments across the GTA.

The assignment sales market has collapsed alongside the broader condo sector, with units selling 10-30% below original pre-construction prices. Investors who purchased pre-construction units in 2022-2023 are facing losses of 30-40%, with some Linx condo buyers confronting potential losses exceeding $200,000 per unit. Financing challenges compound these losses, as appraisals are coming in 10-30% below agreed purchase prices, forcing buyers to cover substantial gaps or walk away from deals.

The financial strain on developers stems from multiple factors: construction costs rising 20% year-over-year, interest rate increases creating financing challenges, pre-construction sales hitting 28-year lows, and cost overruns exceeding budgets by hundreds of millions on major projects. Smaller and mid-sized developers with limited cash reserves and heavy reliance on pre-sales for project funding have proven most vulnerable to these market conditions.

Historical buildup reveals decade-long speculation cycle

The current crisis represents the inevitable correction of imbalances that built systematically from 2015-2022. The foundation was laid during the 2015-2017 period when the Bank of Canada cut rates to emergency levels following the oil price crash, creating an ultra-low borrowing cost environment that fueled asset price inflation. Pre-construction condos, which historically traded below resale prices, reached price parity around 2010-2011 and thereafter commanded premium pricing.

The assignment flipping market reached industrial scale during this period, with some investors holding dozens of units simultaneously. By 2019, Statistics Canada estimated that one-third of the Toronto condo market was owned by non-residents who either rented out units or left them empty, while domestic investors comprised another significant portion of demand.

Government policy responses proved insufficient to address the growing speculation. Ontario's introduction of the 15% Foreign Buyer Tax in April 2017 had immediate psychological impact but failed to address the broader speculation dynamics. The tax was increased to 20% in March 2022 and then 25% in October 2022, while a federal foreign buyer ban was implemented in January 2023. However, these measures came after speculative dynamics were already deeply embedded in market structure.

The pandemic period from 2020-2022 accelerated rather than corrected these imbalances. Emergency rate cuts to 0.25% in March 2020, combined with massive fiscal stimulus, supercharged speculative activity. Pre-construction downtown condos reached $1,700 per square foot by mid-2022, while the assignment market operated with VVIP access and specialized agents facilitating rapid resales of pre-construction units.

The interest rate shock beginning in March 2022 exposed the unsustainable debt levels underlying the market. Ten consecutive rate hikes bringing the overnight rate from 0.25% to 5% created immediate financing stress for leveraged investors and developers. Toronto average condo prices declined 17% from March to July 2022, while sales dropped 71% from March to December 2022, marking the beginning of the current crisis.

By 2023, CIBC/Urbanation research revealed that 77% of Toronto investors with new condo mortgages were losing money, with average negative cash flows of $597 per month. Carrying costs rose 24% while rents increased only 15%, creating a fundamental shift in investment economics that triggered the investor retreat driving current market conditions.

Experts predict prolonged Toronto condo market adjustment

Major bank economists and industry analysts are remarkably consistent in their outlook: 2025 will bring continued price declines and weak sales, followed by modest recovery beginning in 2026. TD Economics, the most bearish among major forecasters, predicts condo prices will fall an additional 10% in 2025 alone, bringing total declines to 15-20% from the Q3 2023 peak by year-end.

Urbanation President Shaun Hildebrand describes the market as having "entered a phase of the downturn that is really starting to wreak havoc," citing construction starts at their lowest level since 1995 and supply levels seven times balanced market conditions. RBC Economics warns of continued inventory pressure, particularly in Toronto where the sales-to-new listings ratio has dropped to 35.5%—the lowest level since the 2009 recession.

The timeline for recovery reflects the magnitude of current imbalances. BMO Economics predicts Canadian housing prices won't surpass 2022 levels until 2029, characterizing the current period as "prolonged consolidation" rather than temporary correction. However, this extended adjustment period is simultaneously creating conditions for future supply shortages, as current construction collapse will significantly reduce available inventory by 2026-2027.

Policy changes on the horizon may provide modest support. The federal government has pledged to eliminate GST for first-time buyers on homes under $1 million, reduce development charges by 50%, and extend 30-year amortizations to additional buyer categories. Mortgage rule changes in December 2024 increased the insured mortgage price cap from $1 million to $1.5 million, potentially easing financing conditions for some buyers.

However, experts emphasize these measures will have limited impact given the scale of current oversupply. Immigration policy changes reducing annual permanent resident targets from 485,000+ to 365,000 by 2027 will further reduce housing demand pressure, particularly affecting the rental market that has supported some condo investor activity.

The assignment market represents both risk and opportunity according to industry analysts. Ben Myers identifies this as a "fundamental issue for developers in 2025 and 2026" when buyers who purchased at peak pricing must close on their purchases. However, the distressed nature of assignment sales may create opportunities for qualified buyers able to negotiate below current market values.

How is the condo market across GTA municipalities?

Municipal-level analysis reveals significant variations in market performance and development activity across the GTA. Vaughan's VMC district demonstrates the strongest resilience, with condo prices actually increasing 8.6% year-over-year to $655,442, supported by reduced development charges (from $94,466 to $50,193), streamlined approval processes, and strong municipal support for high-density development.

North York has emerged as a relative bright spot within Toronto, outperforming the city core with consecutive monthly price gains. One-bedroom units range from $503,000 to $528,000, while two-bedroom units hit yearly highs at $698,400. The area benefits from excellent transit connectivity and positioning as a "cheaper alternative" to downtown while maintaining urban amenities.

Richmond Hill and Markham face different challenges despite strong development pipelines. Both municipalities are planning massive Transit-Oriented Communities around subway stations, with Richmond Hill's High Tech TOC expecting 40,000+ new residents across 33 towers. However, the scale of proposed density raises infrastructure capacity concerns and municipal planning challenges that may delay project implementation.

Mississauga, as the GTA's second-largest condo market, shows moderate weakness with home prices down 5.0% year-over-year to $1,040,979. Pre-construction activity has significantly slowed, though the rental market remains relatively strong with low vacancy rates providing some investor support. Infrastructure strain around Square One limits new high-density approvals despite strong transportation connectivity.

Brampton faces the most significant structural challenges, with home prices down 5.1% year-over-year and limited pre-construction condo development. Transit connectivity limitations and infrastructure capacity concerns constrain the municipality's ability to attract condo development, though affordability advantages may support longer-term growth potential.

Future supply crisis emerges from current construction collapse

While the current market faces severe oversupply, the dramatic reduction in construction starts is creating conditions for acute housing shortages by 2026-2027. Construction starts fell from 18,950 units in 2023 to just 9,258 in 2024, representing a 51% decline that accelerated to an 88% drop below 10-year averages in Q1 2025.

The construction pipeline shows a dramatic future supply cliff. After record completions of 31,396 units expected in 2025, completions are projected to fall to 17,487 units in 2026 and potentially below 10,000 units annually by 2028. This represents the most severe construction decline since reliable records began, with implications extending well beyond the current correction cycle.

The employment impact is already substantial, with an estimated 35,000 construction jobs lost as the number of active projects dropped from 206 to 135. This employment effect will compound the economic challenges facing the broader GTA economy and may influence the timing and strength of eventual market recovery.

Developer behavior suggests the supply shortage will be severe. Only 22 projects launched in 2024 compared to 69 in 2023, while Q1 2025 saw just 2 projects launch totaling 275 units. Many developers are shifting to purpose-built rental construction, which will not address the ownership supply shortage building for the latter part of the decade.

So what's next for the GTA Condo Market?

The Toronto GTA condo market crisis represents the most significant housing market correction in over 30 years, with fundamental supply-demand imbalances requiring years to resolve. The current oversupply situation will likely persist through 2025, creating opportunities for well-positioned buyers but continued challenges for sellers and developers.

For industry professionals, the crisis demands strategic adaptation. Real estate agents must adjust client expectations to current market realities, emphasizing negotiation opportunities and selection advantages for buyers while helping sellers understand the new pricing environment. Developers face difficult decisions about project timing, with many choosing to delay launches until market conditions improve or converting planned condominiums to rental properties.

Potential buyers benefit from unprecedented selection and negotiation power, but should carefully evaluate financing capacity and long-term holding intentions. The assignment market may offer value opportunities for sophisticated buyers able to navigate complex legal and financing structures, while traditional resale properties provide immediate occupancy advantages.

The market's eventual recovery will likely be gradual rather than sharp, dependent on successful rebalancing of supply and demand fundamentals rather than speculative dynamics. Policy support may provide modest assistance, but the scale of current imbalances requires time and reduced supply to correct. Industry participants who understand these dynamics and position appropriately for the extended adjustment period will be best positioned to benefit from the eventual market normalization expected in the latter half of the decade.

Unlock Your Seamless Closing Experience

Your Journey to a Worry-Free Closing Starts Here!