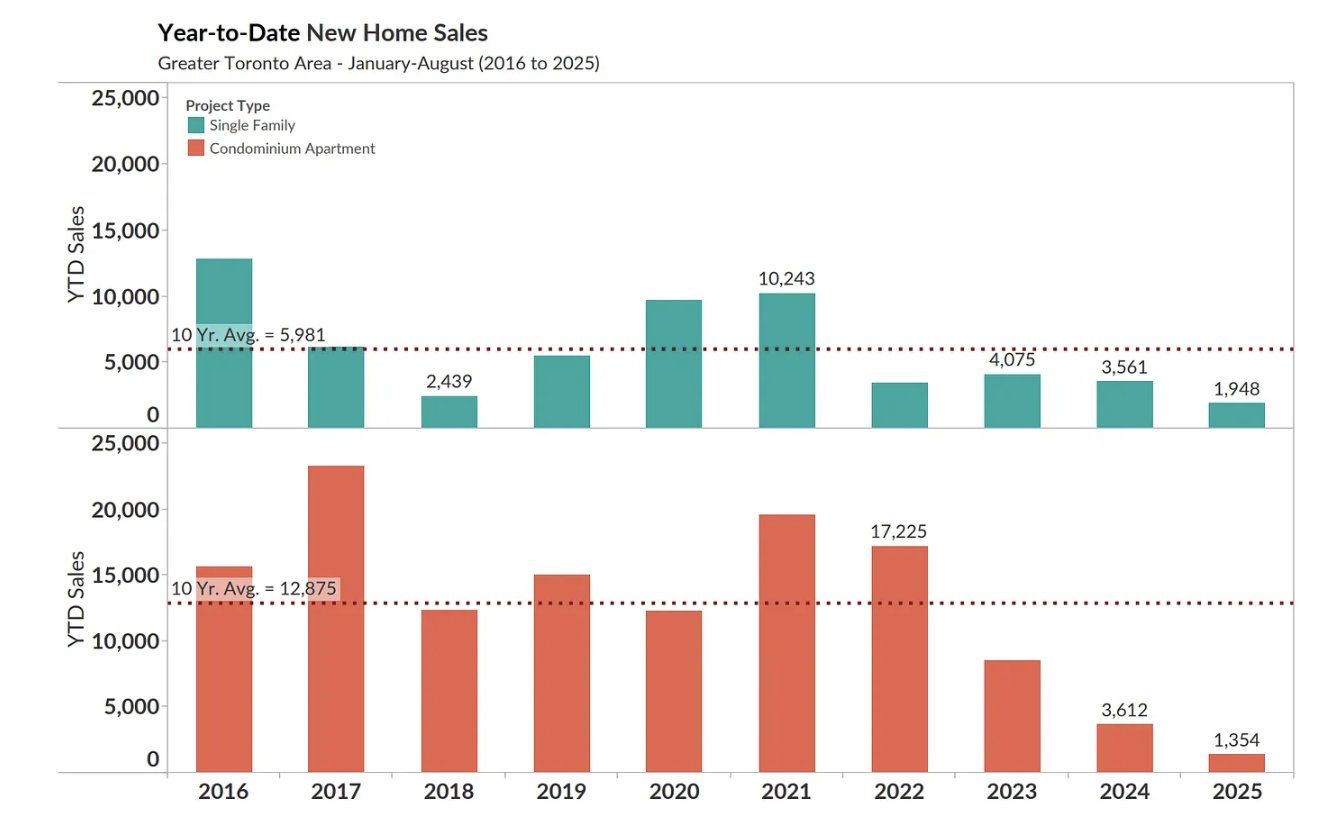

The Greater Toronto Area's new home market has experienced a dramatic downturn, with 2025 sales tracking at historic lows. Through August 2025, only 1,948 single-family homes and 1,354 condominium apartments have sold, representing drops of 67% and 92% respectively compared to the 10-year averages.

These aren't just bad numbers; they're catastrophic.

Why have new home sales collapsed in Toronto?

Interest Rate Shock

The primary culprit is the Bank of Canada's aggressive interest rate hiking cycle that began in 2022. Rates jumped from near-zero to over 5% in less than two years, fundamentally changing affordability calculations for buyers. A mortgage that was manageable at 2% became unaffordable at 5.5%, instantly pricing out huge segments of potential buyers.

How did affordability deteriorate so quickly?

Consider this: a buyer with a $900,000 mortgage at 2% pays roughly $3,300 monthly. That same mortgage at 5.5% costs approximately $5,100 monthly, a 55% increase. For new homes, which command premium prices, this math became impossible for most buyers. The combination of high prices (which had surged during the pandemic) and high rates created a perfect storm of unaffordability.

Why are condos performing even worse than single-family homes?

Condominium sales have been hit particularly hard, down 92% from their 10-year average. Several factors explain this:

Investor Withdrawal: Condos have traditionally attracted investors, but negative cash flow has driven investors to the sidelines. Research revealed that 77% of Toronto investors with new condo mortgages were losing money, with average negative cash flows of $597 per month. Why would an investor buy when they're losing money every month?

Condo Fee Concerns: Rising insurance costs and building maintenance have pushed condo fees higher, adding hundreds of dollars to monthly carrying costs. Buyers are increasingly wary of these unpredictable expenses.

Work-From-Home Shift: The pandemic permanently changed where people want to live. Smaller condo units in dense urban cores became less appealing when people needed home offices and more space.

What role did oversupply play?

The 2017-2021 period saw unprecedented condo construction in Toronto. Developers launched thousands of units during the low-rate environment, many of which are completing now. This surge in supply is meeting the market at exactly the wrong time, when demand has evaporated. The result? Units sitting unsold, developers offering incentives, and investors underwater on pre-construction purchases.

Why aren't prices falling more dramatically?

This is the paradox observers struggle with: if sales are down 90%, why aren't prices crashing? Several factors explain the sticky pricing:

Builder Economics: Developers have land costs, construction costs, and financing costs baked in. Selling below certain thresholds means taking losses, which they'll avoid through slow sales rather than fire sales.

Lack of Distressed Selling: Unlike existing homes, new developments aren't subject to the same foreclosure dynamics. Builders can slow releases or hold inventory rather than capitulate on price.

Selective Completions: Some developers are delaying project launches or slowing construction to avoid flooding an already oversupplied market.

What does this mean for the broader Toronto economy?

Construction Slowdown

New housing starts have plummeted as developers react to poor sales. Construction starts fell from 18,950 units in 2023 to just 9,258 in 2024, representing a 51% decline that accelerated to an 88% drop below 10-year averages in Q1 2025. This ripples through the entire construction ecosystem, trades, suppliers, and professional services, representing thousands of jobs and billions in economic activity.

Municipal Revenue Impact

Development charges and property taxes from new construction represent significant municipal revenue. The slowdown means budget pressures for cities already struggling with infrastructure demands.

Rental Market Pressure

Paradoxically, while condo sales collapse, rental demand remains strong. Many units intended for owner-occupancy are becoming rentals, but not enough to ease Toronto's rental crisis. The investment math that works for established landlords doesn't work for new buyers.

When will the market recover?

The recovery depends on several variables aligning:

Interest Rate Trajectory: The Bank of Canada has begun cutting rates, but mortgage rates remain elevated. A return to the 3-4% range would significantly improve affordability and buyer sentiment.

Immigration Policy: Canada's high immigration targets drive underlying housing demand, but newcomers typically rent first. The conversion from renters to buyers takes time and income growth.

Price Adjustments: Either prices need to fall or incomes need to rise substantially. The gap between what people can afford and what homes cost must narrow.

Sentiment Shift: Markets are psychological. Even when fundamentals improve, buyers need confidence to return. After being burned by rapid rate increases, many potential buyers remain cautious.

What should buyers, sellers, and investors know?

For Buyers: This is a buyer's market for new construction. Developers are negotiating, offering incentives, and carrying more inventory than they'd like. Those with secure financing and long-term horizons have leverage they haven't had in years.

For Developers: The cycle has turned decisively. Projects that made sense at 2% rates don't work at 5%. Expect a period of industry consolidation, project cancellations, and a return to more conservative underwriting.

For Investors: The easy money has been made. Buying pre-construction and flipping on assignment, a strategy that worked brilliantly from 2015-2021, now carries substantial risk. Many investors are trapped in negative cash flow situations.

Is this the new normal?

Toronto's housing market has experienced cyclical downturns before (1989, 2008, 2017) but always rebounded. However, each cycle is different. The current downturn combines interest rate shock, affordability crisis, demographic shifts, and supply oversupply in ways that feel unprecedented.

The 10-year averages shown in the chart (5,981 single-family homes and 12,875 condos annually) may not be achievable benchmarks for years to come. A more sustainable market might operate at lower volumes with more realistic price-to-income ratios.

What's clear is that the 2016-2021 period was extraordinary, fueled by ultra-low rates, foreign investment, and speculation. The current correction, painful as it is, represents a return to more fundamental market dynamics. The question isn't whether Toronto's market will recover, but what that recovery will look like and how long it will take.

What does the future hold for Toronto housing?

The current market collapse is creating the foundation for a severe housing shortage by 2026-2027. After record completions expected in 2025, completions are projected to fall dramatically. This represents the most severe construction decline since reliable records began, with implications extending well beyond the current correction cycle.

Recovery will be gradual and regionally different, with three key factors determining when markets improve: interest rates need to stay low, trade problems with the US need to be fixed, and the right balance of homes for sale needs to be achieved. Market experts predict recovery beginning in late 2026 with more robust activity in 2027, though Toronto and Vancouver will take longer than other Canadian markets.

Unlock Your Seamless Closing Experience

Your Journey to a Worry-Free Closing Starts Here!