Toronto's condominium market entered 2026 in its deepest correction in over three decades.

Prices have fallen to levels not seen since 2021, sales volumes continue to crater, and a wave of completed but unsold inventory is reshaping the landscape for buyers, sellers, and investors alike. Meanwhile, a frozen pre-construction pipeline is quietly setting the stage for a supply crisis later this decade.

Here's what the latest data tells us and what it means for anyone navigating the Toronto condo market right now.

Key Takeaways: January 2026

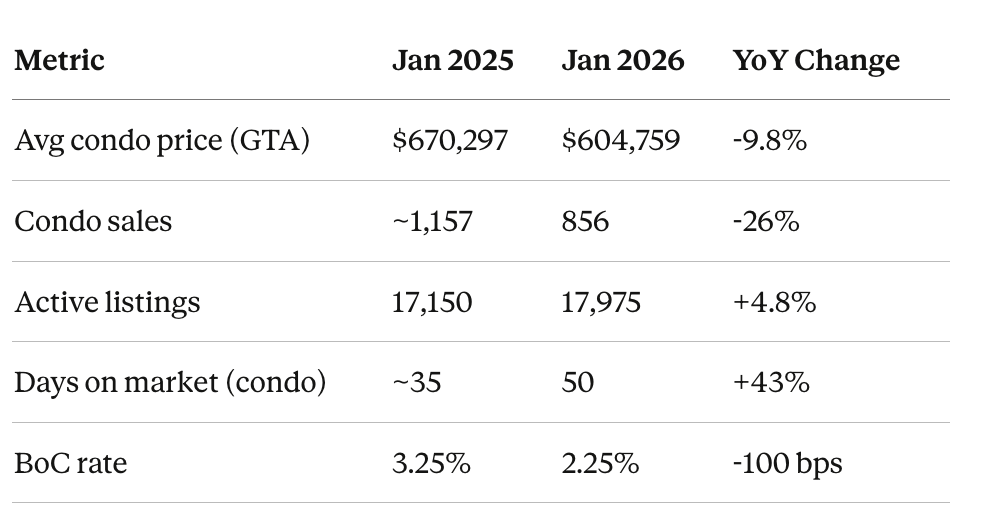

- Average GTA condo price: $604,759 (down 9.8% YoY)

- Condo sales: 856 transactions (down 26% YoY)

- Active listings: 17,975 (up 4.8% YoY)

- Average days on market: 50 days (condos)

- Bank of Canada rate: 2.25% (holding steady)

- New condo sales in 2025: 1,599 units (lowest since 1991)

Prices Have Fallen Sharply and Condos Are Leading the Decline

The average selling price of a condo apartment in the GTA fell to $604,759 in January 2026, down 9.8% year-over-year — the steepest decline among all property types. In the City of Toronto (416 area code), the average condo price came in at $631,932, while condos in the 905 suburbs dropped to $551,166.

To put this in context, the average GTA home price overall fell below the $1 million mark for the first time since January 2021, landing at $973,289 — a 6.5% year-over-year decline. But it's the condo segment that's bearing the brunt of the correction. Prices are now roughly 14–20% below their Q1 2022 peak of approximately $790,000, depending on the segment and geography.

The MLS Home Price Index (HPI) Composite benchmark was down 8% year-over-year in January 2026, underscoring that this isn't just an averaging effect. Actual price levels are falling across the board.

Sales Volumes Continue to Crater

There were 3,082 home sales reported across the GTA in January 2026, down 19.3% compared to January 2025. But condos got hit hardest, with condo apartment sales sliding 26% year-over-year, the steepest decline of any property type.

The condo sector recorded just 856 total sales, with the City of Toronto accounting for roughly 66% of transactions (568 sales). The 905 suburbs saw condo sales plunge by 30.3%. This is the biggest drop of any segment in the region.

Several factors compounded the slowdown in January: beyond the usual post-holiday lull, Toronto experienced two major snowfalls and extended stretches of freezing temperatures that suppressed showings and delayed listings. But the weather only partly explains the weakness. Buyer sentiment remains cautious amid trade uncertainty, layoff fears, and the lingering effects of a market that still hasn't found its floor.

Inventory Is Elevated and Properties Are Sitting Longer

Active listings across the GTA stood at 17,975 in January 2026, up 4.8% year-over-year, even as new listings entering the MLS system actually declined 13.3% compared to last January. That tells you something: properties are sitting on the market longer, accumulating into a growing pool of unsold inventory.

The average days on market for Toronto condos reached 50 days, up from the mid-30s a year ago. Across all property types, the average property took 67 days to sell, up from 55 in January 2025.

The sales-to-listing ratio has shifted firmly in buyers' favour.

The average sales-price-to-listing-price ratio fell to 97% meaning homes sold for 3% below asking, on average compared to 99% in January 2025. For condos specifically, the picture is even more buyer-friendly, with the sector posting a sales-to-new-listings ratio of just 29.2% in 2025, well below the threshold of a balanced market.

The Completion Wave Continues But the Pipeline Is Drying Up

One of the defining dynamics of this market cycle is the record-breaking wave of condo completions flooding the market at exactly the wrong time. According to Urbanation, 29,291 condo units were completed in 2025, nearly matching the 2024 record of 29,924 and running about 50% above the 10-year average.

Completions are expected to decline to roughly 22,066 units in 2026 and then drop sharply to 14,366 units in 2027. By 2029, Urbanation says virtually no new condos are expected to be delivered. A staggering projection that reflects the near-total collapse in construction starts over the past three years.

Here's the math behind that collapse:

- New condo sales in the GTHA fell for the fourth consecutive year in 2025, plunging 60% from 2024 to just 1,599 units — the lowest annual total since 1991 and 91% below the 10-year average.

- Condo construction starts totalled just 3,272 units in 2025, an 88% decline over three years.

- A record 28 condo projects totalling 7,243 units were cancelled in 2025, more than doubling the units cancelled in 2024 and surpassing the previous record set in 2018.

- As of year-end 2025, there were 3,897 completed and unsold condo units — up 131% from a year earlier and five times higher than 2023 levels.

- An additional ~3,000 units (roughly 10% of pre-sold condos registered in 2025) were taken back by developers after purchasers failed to close.

The paradox is clear: the market is simultaneously oversupplied today and heading toward a severe shortage by the end of the decade. The current glut of completions will eventually give way to a supply drought — but that adjustment is likely years away. For pre-construction buyers facing appraisal shortfalls at closing, we've covered your options when dealing with an appraisal gap.

The Rental Market Is Tenant-Friendly

Toronto's condo rental market continues to soften, compounding the challenges for investor-owners who make up a significant share of the condo ownership base.

Average rents are declining, with condo apartment rents down approximately 5.7% year-over-year nationally as of January 2026. In Toronto, the average unfurnished one-bedroom rent fell to $1,993/month, down $156 year-over-year. Two-bedroom asking rents hovered around $2,800.

The purpose-built apartment vacancy rate in Toronto hit 3% for the first time since the pandemic, and condo rental vacancies are climbing as well. TRREB data shows that while rental transactions grew 16% year-over-year in Q4 2025 (reaching 13,687), rental listings grew by 8.5% — and average rents still fell across all market segments.

The dynamic driving this: weak ownership market conditions are pushing more condo owners to list their units for rent rather than sell at a loss, flooding the rental market with additional supply. This is a rational individual decision that, in aggregate, is putting further downward pressure on rents and investor cash flows.

CIBC and Urbanation research found that 77% of Toronto investors with new condo mortgages were losing money on a cash-flow basis, with average negative cash flows of $597 per month. That calculus hasn't improved meaningfully, and it's a major reason investor demand for new condos has essentially evaporated.

Interest Rates: Cuts Are Done (For Now)

The Bank of Canada held its policy rate steady at 2.25% on January 28, 2026, marking the second consecutive pause after nine rate cuts between June 2024 and October 2025 that lowered the overnight rate by a total of 275 basis points (from 5.00%).

Current mortgage rates reflect this lower-rate environment: the best 5-year fixed rate sits around 3.69%, and the best 5-year variable rate is approximately 3.35%. These are significantly more favourable than the 6%+ rates that prevailed in late 2023 and early 2024.

However, these lower rates have not yet translated into meaningful demand in the condo market. Several headwinds are counteracting the rate relief:

- Trade uncertainty: U.S. tariffs on Canadian goods — particularly lumber, steel, and aluminum — are raising construction costs and damaging business confidence. This uncertainty is keeping many buyers on the sidelines.

- Mortgage renewals: Approximately 33% of Canadian mortgage holders are expected to face higher monthly payments by end of 2026. For fixed-rate borrowers renewing this year, payment increases are expected to average around 20%.

- Weak consumer confidence: TRREB's annual Ipsos survey found that GTA homebuying intentions for 2026 declined by five percentage points compared to 2025, to just 22%, despite improved affordability.

- Job market concerns: Rising unemployment and tariff-related layoff risks are tempering demand, particularly among the move-up buyers and investors who have traditionally driven condo activity.

What This Means for Different Market Participants

If You're a Buyer

This is objectively one of the most buyer-friendly condo markets in decades. Prices are at multi-year lows, inventory is elevated, properties are sitting longer, and sellers are negotiating. The average condo is selling for 3% or more below asking price, and the selection is broader than it's been in years.

First-time buyers are particularly well-positioned. TRREB's survey shows that 45% of intending homebuyers in 2026 will be first-time buyers, and affordability has meaningfully improved — the average monthly mortgage payment for a benchmark home is projected to decline in 2026 for the first time since 2020.

The risk, of course, is that prices haven't finished falling. If the trade war escalates or the economy weakens further, there could be additional downside. But for buyers with a long time horizon and stable employment, the entry points are attractive relative to where the market has been. (And if you're getting ready to close, make sure you've budgeted for closing costs.)

If You're a Seller

This is a challenging environment. Expect longer days on market, more buyer negotiation power, and the need to price competitively from the start. Overpriced listings are being punished in this market — the gap between asking and selling prices is widening, and stale listings erode leverage quickly.

If you can afford to wait, market conditions may improve in the second half of 2026 as excess inventory is absorbed and the pipeline of new completions begins to shrink. But a return to 2022 peak prices is likely years away.

If You're an Investor

The investment case for Toronto condos remains difficult in the near term. Negative cash flows persist for most leveraged investors, rental growth is negative, and capital appreciation is working against you. The investors who are surviving this cycle are those with low leverage, long time horizons, or the ability to absorb short-term losses.

However, the collapsing development pipeline does set up a compelling medium-to-long-term thesis. With new condo starts down 88% and virtually no completions expected by decade's end, supply constraints will eventually reassert themselves. The question is timing — and most analysts suggest a meaningful recovery in investor returns is more likely a 2028+ story. If you're currently holding a pre-construction unit and weighing your options, we've also covered the realities of selling an assignment in this market.

If You're a Renter

You have more leverage than you've had in years. Rents are declining, vacancies are rising, and landlords are competing for tenants. If your lease is coming up for renewal, it's worth shopping the market, you may find better value, and your current landlord may be willing to negotiate to avoid a vacancy.

Outlook: Bottoming Out, But Not Bouncing Back

The consensus view from major banks, TRREB, and industry analysts is that Toronto's condo market is in the process of bottoming out — but a quick rebound is unlikely.

TRREB forecasts that the GTA average home price will range between $1 million and $1.03 million for 2026, with prices likely lower year-over-year in the first half before stabilizing in the second half. RBC Economics expects that condo inventory could begin declining in early 2026, with conditions gradually improving through the year and setting the stage for renewed pre-construction demand in the second half of 2026 and more robust activity in 2027.

The wildcard remains the trade environment. Escalating tariffs could delay recovery by further dampening confidence and increasing construction costs. On the other hand, if trade tensions de-escalate, the combination of lower rates, improved affordability, and pent-up demand from sidelined buyers could accelerate the stabilization. Federal housing policy is also a factor to watch, the newly launched Build Canada Homes initiative and the post-election policy landscape could provide additional tailwinds if executed effectively.

What's clear is that the structural forces shaping this market, a record wave of completions meeting weak demand, followed by a pipeline collapse that will create future scarcity are playing out in real time. For market participants willing to look beyond the current weakness, the seeds of the next cycle are already being planted.

Unlock Your Seamless Closing Experience

Your Journey to a Worry-Free Closing Starts Here!